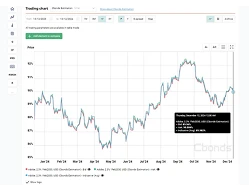

HW00 Global High Yield Index, Spread-Govt

diario

bps

Valor anterior

entidad de cálculos: BofA Securities

Últimos datos al 29/07/2026